Now that you have made your decision about where to attend graduate school, it is time to figure out how you are going to pay for it. This can be a daunting process, but with a good strategy and help from your school's financial aid office, it doesn't need to hinder your studies. It is possible to keep your expenses to a minimum during school and to repay your loans later without going broke.

Before enrollment

Once you are accepted, the university's Financial Aid office will send you a financial aid package based on your

Federal Application for Federal Student Aid (FAFSA) report. The FAFSA consists of a questionnaire about your personal and family finances, your background, and your education expectations. Your "need" for student aid is then calculated, and the FAFSA report is sent to your target college(s), which offer you an aid package. You may discover that you will need more or less than what is offered. Once you get your financial aid offer, it's time to figure out how much money to borrow and to write up a budget.

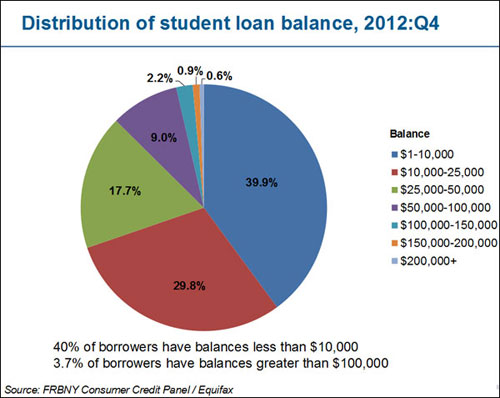

More loan-related resources

In addition to the links in the text, here are a few other resources that can help you understand the world of graduate education loans.

The student life or financial aid offices at many universities publish sample budgets for their students, which can be helpful in designing your own. Here is a sample budget that can help you make your own:

It is important to outline a personal budget for yourself for the entire time you are expected to be in school. Your budget should include all expected expenses and income, so you can estimate how much you will need to seek in loans and other aid. This sample budget can help you plan your financial outlook; your target school may offer a sample budget with program-specific costs on its website. Sample budget templates can be found online that account for various other expenses typically encountered by grad students.

A good loan strategy starts with minimizing the amount you need to borrow (the principal). Remember, the less you borrow, the less you pay back in interest. If you were a very good student as an undergraduate, planning on studying a high-need subject, or are a member of an underrepresented population, apply for all the scholarships you can that are offered by your university and by private or public organizations. Seek employment at the university as a teaching or research assistant. Many schools will remit (waive) your tuition and/or provide you a stipend that will drastically reduce the cost of your education.

If you are awarded any scholarships, grants, or assistantships, calculate the income in your budget, and borrow an equivalent amount less as a principal. Even if you can get a high loan amount, take out the bare minimum and live as frugally as possible. Your post-graduate self will thank you later.

Action steps:

- File a FAFSA report so that you can start the financial aid process.

- Develop a personal budget reflecting your income and expenses for the full anticipated length of your graduate studies.

- Use your budget to determine the minimum possible principal you should take in student loans.

While enrolled

The best way to limit your loan debt is to be an excellent student. Do what you can to get good grades, be active on campus, and create good relationships with your professors and advisors. This will go a long way toward making you more competitive for scholarships, grants, and assistantships. If you didn't get any financial aid aside from loans your first year, you can use your new, improved standing on campus as a foundation to compete for awards in the next year.

As long as it doesn't negatively affect your studies, get a part-time job to help cover your expenses. It may certainly be possible to subsist on your loans, but the income from a job will greatly reduce the financial stress of the debt after graduation. If you have many expenses, attending grad school part-time and working full- or part-time might be your best option. Paying for school up front is much cheaper in the long run than paying with loans, so be smart about how much loan debt you can really handle.

After graduation

Armed with your advanced degree, it's time to land that fulfilling job with a good salary. It's also time to pay back the thousands of dollars you owe to your lenders.

Some federal loan programs forgive (cancel) your debt if you work in a certain areas of public service (see our article on navigating student loans). Perkins loans (PDF) may be cancelled for a variety of circumstances detailed in the cancellation request. Teachers who practice in specific low-income districts or teach high-need subjects may have their federal loans forgiven. Federal loans can also be deferred while you fulfill volunteer term-of-service programs such as Peace Corps or AmeriCorps, easing your financial obligations during low-income volunteer service. Ask your financial aid advisor about these loan forgiveness or deferment options during your exit counseling upon graduation.

If it helps reduce your interest rate, consolidate your loan debt with any undergraduate debt you still have, and make one monthly payment instead of several. If you have several federal loans, you can also consolidate those into one loan, which may make repayment easier and give you a longer repayment term. Private loans can be consolidated as well, but be sure to shop around for the best rates and incentives—remember that banks will be competing for your business. Talk to your financial advisor or student aid office about loan consolidation for more in-depth advice.

Figure out how much you can realistically pay back each month based on your expected income. Try to pay back your debt as a percentage of your income. If you get a higher paying job two years out of school, adjust your repayment accordingly. This way, you will pay it back faster and pay less interest over the life of the loan.

Conclusion and further resources

Being financially savvy during grad school requires restraint and foresight. If you're invested enough in your professional future to take on the considerable expense of grad school, you should be sure to budget and limit debt as intelligently as possible. Chase scholarships, assistantships, and fellowships, while also increasing your chance of getting them by excelling in your coursework. While it's no guarantee, the best way to keep school cheap is to be a good student. After you graduate, learn more about managing your education debt.

")

")

")

")

")