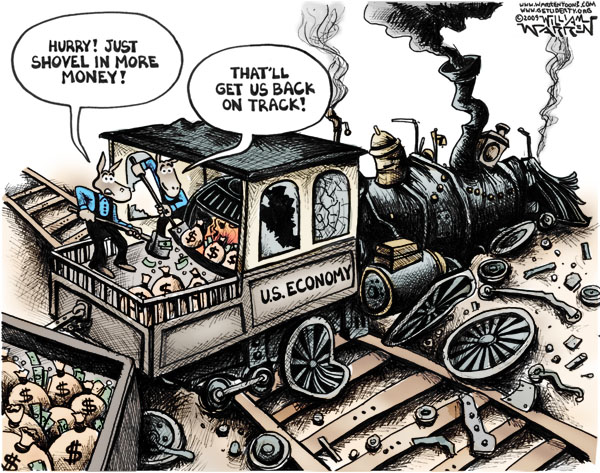

That’s how Americans for Limited Government (ALG) President Bill Wilson described the latest scam by government and financial institutions to boost “growth.” Having exhausted the market for crappy loans in housing and college students, now banks are turning their attention to the rapidly growing industry of subprime auto loans — that is, loans to borrowers with bad credit, yielding higher interest rates, and are more likely to default. |

Car loans you can’t afford the next subprime

Actual auto expenses or standard mileage rate? Which business deduction method will cut your taxes more?

Has all the attention given Google's driverless car got you thinking about your auto? If you're a business owner, it could be the perfect vehicle.

It has no steering wheel, accelerator or brake pedal to mess with. You use your smartphone or tablet app to summon the vehicle, set your route, get in and go. Then just sit back and enjoy as the Google machine takes you to your destination.

If it's to a business meeting, you can use the time you otherwise would be driving to polish your presentation. Or you can call your spouse to ask him or her to pick up dinner or the cleaning or the kids. Or you can just relax so you'll be in the best frame of mind for your important professional encounter.

More Pinoys Purchase a New Car with help from Financing

In the first quarter of this year, Bangko Sentral ng Pilipinas (BSP) reported that auto loans increased by 26% to P244.61 billion from P194.37 billion the previous year.

The demand for car loans in the Philippines will continue to increase as more Pinoy car buyers see financing as a better option when purchasing a new car, Carmudi said.

In its recent study, the company reported on the growth of car financing in the Philippines as well as other emerging markets. The white paper entitled “Car Financing in the Philippines” provides a look into the current and future state of car financing and how consumer attitudes toward credit have changed in recent years.

5 Ways To Pay Off Your Car Loan Sooner

Getting rid of debts like car loans sooner rather than later can be a solid investment in your future for a number of reasons. It not only improves your credit history, but means more money in your bank account, so if you’re lumbering away under the cloud of debt, here are five ways to ease the burden and help pay off your car loan sooner.

5 Financial Tips for Recent College Graduates

As a recent college graduate, I know how intimidating personal finance can be. Fortunately, there is a wealth of (free) knowledge online to serve as a starting point for a sound financial education. Here are a few tips I've gathered from friends, family, experience, and online resources to help college graduates (and non-graduates) from any background.

1. Maximize savings on large, recurring payments

There are dozens of sites and apps to help you navigate and keep track of spending – personally, I like Mint.com. Take a good look at your credit and debit card spending and calculate where your money is going as a percentage of your total spending. The biggest portions are your heavy-hitters: rent, food, insurance, loan payments, transportation, etc. Rent is commonly the single most expensive bill you will have to pay on a monthly basis. Keep in mind that it may be unwise to pay more than about one-third of post-tax income on rent. First, be open to trade-offs. The apartment that you're touring may not be in your dream neighborhood, but let's say it's $200 cheaper per month and transportation is only $40 more per month. That's nearly $2,000 in net savings per year. Second, sign a longer-term lease. A year-long lease is generally given at a lower rate per month than a shorter-term lease. If you were able to live in a college dorm room for a year, you can sign for an apartment for a year. Research your own heavy-hitters and look to reduce them where possible.

The Student Loan Scam

Full disclosure: I am currently paying federal student loans that I obtained while in college. I never finished college and it was never a huge amount (about $6000), nor do I expect any kind of reform to ever benefit me, but it would be unfair to say I’m a completely disinterested party.

That said, student loans are big business in the United States. The federal government makes over $40 billion in profits on student loans annually, to say nothing of what private firms make. There is currently more than $1.2 trillion in outstanding student loan debt. To put that in perspective, the total amount of all credit card debt in the US is about $900 billion. It’s not a small amount of money.

8 Ways to De-Corporatize Your Money

1. Ditch the Cards

All electronic transactions siphon money out of your community to some extent, so try the human approach and bank in person. Pay in cash or, second best, write a check. If you have to use plastic, choose debit. Your local merchants lose some of their profit any time you use a card, but they pay up to seven times more in fees when it’s a credit card. And studies show people spend 12 to 18 percent more when they use cards instead of cash.

2. Move Your Debt

Already broke up with your mega-bank? From credit card balances to car loans to mortgages, mega-banks make far more money off your debt than your savings. Refinance your debt with a credit union or local bank and let your fees support your community. Be wary of “affinity credit cards,” which donate a certain amount per purchase to good-hearted organizations but often are connected with a mega-bank.

5 Ways to Make Your Dollars Make Sense

Americans’ long-term savings in stocks, bonds, pension, life insurance, and mutual funds total about $30 trillion. But not even 1 percent of these savings touches local small businesses, the source of half the economy’s jobs and output. Is it possible to beat Wall Street’s 5 percent long-term performance by investing in your community? The answer is a resounding yes!

Co-op members who lent to the Weaver Street Market in North Carolina and to the Seward Co-op in Minneapolis earned well over 5 percent per year. Many outside investors who bought preferred shares of the Coulee Region Organic Producers Pool, a co-op of organic farmers, are still receiving an annual dividend of 6 percent. Equal Exchange has paid a dividend to its preferred shareholders averaging above 5 percent for 22 years. Investors who participate in New Markets Tax Credits automatically get a tax credit equal to 5 percent of their capital for each of the first three years and 6 percent for the next four—even if the investment generates no real return whatsoever. Burt Chojnowski’s returns have been good enough to convince outside investors to put more than $300 million into his local companies and projects over 25 years in Fairfield, Iowa. Most of LION’s deals in Port Townsend, Washington, are paying between 5 and 8 percent returns per year. Microlenders on Prosper.com are averaging an annual return of 10.4 percent. Jeff Haugland has paid the local shareholders of Community Grocers in Mount Ayr, Iowa, an annual dividend of 5.25 percent.

Buying a New Car fo Back to School? Some Tips to Consider!

Labor Day is approaching quickly, coeds are off to school, and summer car buying season is in full swing - with current auto loan interest rates holding steady in the low 4%,(1) consumers are regaining confidence in the economy,(2) and venturing to dealerships looking to take advantage of late 2013 vehicle model deals.

The decision to purchase a vehicle involves a number of budget considerations, and CarFinance.com has created key tips to empower consumers with detailed budget know-how throughout their vehicle selection process- they are especially important for college students, who may be living on their own for the first time!.

Items to calculate before signing on the dotted – or electronic – line:

Are Online Cash Stores More Expensive Than Offline Stores?

Online cash stores offer a variety of rates. More often than not, they are less expensive than offline stores. Of course there are companies that offer extremely high rates, but you can avoid them if you shop around. In fact, that is one of the biggest advantages to online stores – you can compare rates in minutes to find the lowest finance fees.

Fees To Look For

Most cash stores charge a flat fee rather than a percentage of your payday loan. Some online cash stores also charge an application fee. By shopping around you can find lenders who don’t charge this. And some of these lenders will waive the fee for first time borrowers.

When you are comparing fees, you should look at the APR or annual percentage rate. This number is what the loan would cost if you carried it for an entire year. While most customers make their payment in less than a month, the APR allows you to make quick comparisons.

Watch Out For High Rates

Don’t sign up for the first cash advance offer you get. Shop for rates first. You can do this by calling around, but an easier way is to look up rates on line. You can find the APR or fees either under ‘Fees’ or the ‘FAQ’ section. If you can’t find numbers to compare, email the company.

You also want to pay attention to how long the loan fees are for and make sure you compare the same numbers. For instance, if you need a cash advance for 14 days, look at the finance fees for the 14 day period with each lender.

Understand Payment Plans

Another way lenders can take advantage of your situation is by delaying your payments. Lenders who only deduct the minimum payment rather than the total amount will charge you more in finance fees. Initially these lenders may have low rates, but by adding more time to your loan, you rack up finance charges.

If you choose to go with one of these lenders, make sure you set up a full payment on your payday. That way you will pay the minimum finance fees, keeping money in your pocket.

source:finance-slot.blogspot.com

Check Into Cash

What are Cash Advance Services? There are plenty of reasons that a person might need a little extra money from time to time, and there are plenty more reasons that they can't wait for their next paycheck to get it, which is why cash advance services may be a convenient alternative.. If you are looking for a way to get a little extra money for unexpected emergencies like car repairs to purchasing needed medicine, a cash advance might be the way to go. So, what are cash advance services? These businesses exist to offer you the cash that you need right now. They take either a personal check or postdated check (depending on state requirements) for the amount that they are lending you, plus a fee, and then they present that check for payment on your next pay period. This is one option to get that much needed cash in advance before your next paycheck. Losing track of when your bill dates can lead to a shortage of cash that otherwise might not have been a problem. When this happens, instead of letting things fall by the wayside until we can pick them up again with our next paycheck, every day people like yourself may opt to visit a cash advance store for the money that we need today. Many people use cash advance center all the time for life's unexpected occurances. As long as you have the money to pay back a cash advance and the fee from your next paycheck, cash advance services may offer a short term solution to money shortfalls between pay periods.

Getting a cash advance online is simple Thanks to the world of online lending, you can now get cash advances online in only a few easy steps.

1. The first step in getting fast cash online is to find a website that offers the service. A simple search engine query will reveal dozens of websites. Some will be big names in the payday loan industry, and others are sure to be smaller, new players in the online lending industry. While the rules and regulations of these lenders might vary, they all work in essentially the same way.

2. You fill out an online application, and once approved, you will receive your money via a direct deposit into your savings or checking account usually by the next business day. Some sites may ask you to prove that you are employed by faxing a copy of your most recent pay stub from work so they can verify how much you make and how frequently you get paid.

3. Once you have been verified, you are ready to have your loan processed. Please be aware, also, that these loans do carry fees. If you cannot repay both the loan and the attached fees, do not complete the application.

4. Payday loans are a great short term financial solution, but if you find yourself short of cash on a regular basis before your next payday, it is best to consult a financial professional to work out a budget you can live with on a regular basis.

5. Keep in mind that payday loan should only be used in emergency situations. Using the funds from a payday loan on expensive gifts, vacations, or other unnecessary items is never a good idea.

6. Getting a cash advance online really is as simple as it sounds. Use it responsibly, and you will achieve the financial solvency you desire.

source:finance-slot.blogspot.com

Cars and Credit Reports

The Problem

I was driving home from the store the other night when I noticed a license plate that made me laugh to myself and then I proceeded to feel sorry for the poor sap driving. The plate read "0 DOWN". It was a white, shiny, new Ford Explorer (probably an 06'). Here's what really got me about the caption: Not only did this consumer purchase a brand new vehicle with no money down, but he was proud of it. DUMB! Commercial advertisements and society as a whole embeds the "Buy Now, Pay Later" method into our heads and it works so well that around 90% of all consumers who purchase new cars do not put $5 down on the vehicle before signing the papers. The sad fact is, is that the average new automobile loses $3,000 as soon as it leaves the lot. Technically, you have gone into debt for something that loses value before you even use it. As if this wasn't depressing enough, the less money you put down on a car and the worse off your credit is, the more you pay for the car. If this isn't one big sand trap I don't know what is!

The Role of Your Credit Report

Your online credit report is affected 2 ways when you buy a new car with no money down. First let's look at the role it plays after you decide you NEED that shiny new sports car. The mass majority of consumers are thinking of one thing when they sit in the 'sales chair' to go through the paperwork: driving the car home (man this is bringing back some bad, bad memories). In order to do this you will need to finance the vehicle which requires pulling up your credit history and your credit report. This can easily be done online right in the sales office while you look around to make sure no one else tries to sneak off with your new toy. The worse off your credit report is, the higher interest rate you will pay. (This is fine though as long as you can still afford to buy food every other week and pay a few bills here and there.) The other role that your credit report plays in this game is the after-effect. The average new car buyer's car payment is 25-30% of their total income. This creates a nice, big road block on your credit report in itself for when you are ready to make another large purchase. Not to mention when you fall behind on even one payment and your credit file takes a hard blow. Try to keep these factors in mind next time the kid in you tries to make a financial decision.

The Solution

Well you're not going to like the best solution but here it is anyway: PAY FOR THE CAR IN FULL! If you saved the car payment every month in a good money market account; not only would you save time and money, but when you walked into the sales office with piles of hundred dollar bills you would get quite a deal! Okay, so you're more likely to win the super lotto than do that right? Well here are a few ideas. As long as you practice a few you might get ahead of this nasty game a little bit or at least protect your online credit report. First, consider getting a 2 or 3 year old car. You can still get a shiny one and the previous owner will have taken the major depreciation of the vehicle passing the savings directly to you. Second, if you can, try waiting and searching to find the best deal possible. Trust me, there is more than 1 of those cars in the market. Third, put something down. Anything! For starters you could put down 10 to 15%. This will lower your monthly payment, lower your interest rate and maybe even cut your payoff time down. Lastly, get a bargain. Don't settle for the asking price by any means. Be patient and keep control of your focus. One definition of maturity is learning to delay pleasure.

source:finance-slot.blogspot.com

Cash Advance - Money When You Need It

So you need money today, but your bank account has seen better days. Perhaps you have an emergency you need to take care of, but the money to do so is nowhere to be found. In both of these situations a cash advance may be just what the financial doctor ordered - a way to get the cash you want today without going through the hassle of dealing with banks and credit card companies.

Cash advances typically come in two flavors: You can get a cash advance that you will pay back at a certain period in the future, with a nominal interest charge; or you can get a cash advance against a tangible asset that you own - say an insurance policy or annuity. Either way, you are getting the money you need today instead of having to wait for weeks (or years) down the road to get it. After all, what good does a $10,000 annuity do you five years from now when you need to get your car fixed today?

There are a number of cash advance organizations out there who will work with you to find the solution that is best for you. Typically, many people utilize the services of a cash advance organization that works much like a bank (without all the hassle): You fill out a small application, they process it immediately and the money is put into your account. The big difference is that, unlike a bank, the entire process is usually over and done in a few minutes!

Typically, cash advance companies will advance you up to about $2,000 - $3,000 depending our your situation and finances. There are some cash advance companies out there that will loan more based on assets you may own that you want to take an advance on. Typically, such assets include things like insurance policies, annuities or lottery payouts. Many times people may hold such "future value" money items, but need the money for them today - after all, what good is money in the future if you may not even be around then to spend it?

Most cash advance companies also offer very flexible repayment options. You can either pay them back in one lump sum, or break the payments up over time. Some cash advance organizations even offer you the ability to pay the loan back through automatic withdrawals from your checking or savings account, making the process even easier. Almost all of them give you the flexibility to determine what date you want the withdrawal to happen on - saving you from having to deal with potential NSF fees.

So if you find yourself a bit strapped for cash, or just want to take a well deserved vacation and need a few extra dollars, consider checking into cash advance services that are offered both online and locally. You'll find competitive rates, great service and most of all the money when you need it without the hassle of dealing with the bank, relatives, credit card companies - and most of all - your mom or dad!

source:finance-slot.blogspot.com

Consolidate Debt – Lead A Debt Free Life!

If you have accumulated innumerable debts over a period of time and are not in a sound financial position, we can lend you a helping hand! We will show you how to get over the debt problems easily. Debt problems if not handled carefully in the initial stages can affect the credit history of the borrower negatively.

To start with, you should look out for a debt consolidation plan online which can help you get a loan at a lower rate of interest. Searching online will help you get the best deal on loans. Also, concentrate on paying back the debts in easy installments.

Debt Consolidation Loan picture by simplydebtsolutions.org.uk

Consolidating debts helps you get a better rate of interest on the loan amount. Any borrower would take up the option of a lower rate of interest than a higher one on the previous one. You should also keep a track of the debts you owe to all your creditors. Start off with making payments by cash for the ones which you can afford to pay quickly.

Debt Management Solutions – Get Over Debt Worries!

Stop worrying now if you are overburdened with mounting debts. We will provide you alternatives to get over them easily. Opt for a debt management solution and reduce your debt burden. Debt management solutions can solve all your problems. Be it the debts, credit card debt, utility bills debt, medical bills debt, or any other debt, we have a solution for all.

You can choose from either a secured debt consolidation loan or an unsecured debt consolidation loan. A secured debt consolidation loan carries a lower rate of interest than an unsecured debt consolidation loan.

A borrower can greatly benefit from a debt consolidation loan. A debt consolidation loan is nothing but a substitute for numerous debts. A borrower can payback the creditor with one single loan fro all the debts and also get a lower monthly payment. He can also get a longer repayment period on the loan.

It is also one of the easiest ways to get over bad credit. A borrower with bad credit history too can benefit greatly by opting for a debt consolidation. It is also the easiest means of improving the financial situation.

source:finance-slot.blogspot.com

| |

Comparing Payday Loan Companies Online

Comparing payday loan companies online saves you time and money. By researching rates, fees, and terms, you can find the best cash advance company. According to federal law, payday loan lenders must post their rates and fees so you can make comparisons.

Researching Rates

Cash advance companies are required to post their rate by an annual percent rate. In other words, they list the lending rate for the whole year. Payday loans are intended to provide a cash advance for a short period, usually just until your next pay period. But if you find you need more time, you can arrange that with your lender.

Listed APR’s do allow you to make quick comparisons of rates since all lender’s have to follow this standard. With a quick check of the numbers, you can find low interest rates. However, that is not the only factor to consider.

Identify Fees

Fees are another way cash advance companies make money. They may come in the form of an application or processing fee. Some lenders will waive this fee if it is your first time using their services. You can also find lenders who don’t charge any fees. These lenders usually charge higher interest rates.

Look for a company that charges low fees. Fees can sometimes cost more than the interest charges. When choosing a payday loan lender, be sure that the interest rates are also low.

Consider Other Factors

You should also consider the convenience of the application process and minimum requirements. There are two types of online applications, fax and no fax. Faxed applications require copies of your picture id, usually a driver’s license, past bank records, and pay stubs. A person will then review your application for approval. A no fax application simply requires you to fill out an application online, which is verified through databases. There is no credit check involved and you can receive a virtually instant approval.

Lenders also vary in their minimum requirements. You may be required to have been employed for two to four months. Other lenders just require you to have a regular income, which could be a social security or pension check. Some lenders check if you have any outstanding checks or payday loans. Others just check that you have an open checking account. So before you sign for your cash advance, check to see that you meet the requirements.

source:finance-slot.blogspot.com

Comparing Secured and Unsecured Loans

Are you, like many people, trying to make sense out of your financial situation? Looking for a way to make ends meet? Struggling to keep up your monthly repayments on credit bills? If so, you might well be tempted by the widespread offers of consolidation loans and other easily available lines of credit, which promise you an end to your financial worries.

|

| Secured and Unsecured Loans , image source : |

Unfortunately, life isn't that simple, and taking out a loan without proper consideration of the consequences can be absolutely disastrous for your future financial health. At the very minimum, you should be completely sure of the kind of loan you're applying for, and what the differences between the types might mean in your particular situation.

There are two major kinds of personal loan, Unsecured and Secured. Here we'll take a brief look at the main features of each, to help you be aware of what you're entering into when signing a loan agreement.

Unsecured Loans

These loans are the most common type, and are what most people think of when considering personal loans. They are usually for small to medium amounts, and are aimed at people with good credit ratings, and the sort of financial circumstances lenders love - a steady income large enough to cover repayments, and no great history of debt problems. To get an unsecured loan you don't have to offer any collateral to guarantee repayment, and so the lenders are looking for someone who represents a low risk. As there is no collateral involved, you don't have to be a homeowner. Rates are often attractive, and compare very favourably with other kinds of unsecured finance such as credit cards.

Secured Loans

These loans are only available to homeowners, as they're advanced on the basis that if you don't keep up repayments, the lender has the option of seizing your home, and selling it to pay off your debt with the proceeds. They are available for much larger amounts than unsecured personal loans, as you may be able to borrow as much as your home is worth or even more, and the repayment term is usually much longer - up to 25 or even 30 years compared to the 5 years which is more common with unsecured loans. Because of the security given to the lender by laying down your home as collateral, the approval criteria are often less strict, so it's easier to be approved, even with a poor credit rating.

Unfortunately this ready acceptance of applicants with adverse credit can mean that the interest rate charged is higher, as the lenders know that most applicants are unable to get finance elsewhere and will be happy to pay a little extra.

So now we've seen the differences and similarities between the two major kinds of loan, but what does it mean in practice? Basically, you should think very hard about turning unsecured debt into secured debt, and you should also consider carefully any attempts made by a lender to upgrade your unsecured loan application into a secured one. After all, defaulting on an unsecured loan will have very damaging consequences for your credit rating, but defaulting on a secured loan would mean losing your home.

source:finance-slot.blogspot.com

Online Cash Stores Vs. Offline Cash Stores

Personal cash loans are essential during emergencies. If there is an unexpected expense such as a utility bill or car repair, most people whip out the credit cards. Because of high finance charges, and the fact that most consumers have little available credit, using credit cards may not be an easy fix. In this case, obtaining a short-term cash advance loan will provide you with the needed cash.

Using Cash Advance Loan Companies

Cash advance companies are financial institutions; however, they operate differently from banks. If you attempt to acquire a personal bank loan, the bank or credit union will pull your credit and lengthen the process to ensure you meet all requirements. Cash advance companies have easy lending requirements. There are no credit checks. Furthermore, you can have funds within a few hours.

Although personal cash advance loan companies approve most loan applications, companies do require applicants to have stable employment and make a minimum monthly income. Moreover, you must have a confirmable checking or savings account to get a cash advance loan.

Payday Loan Company Options

Individuals hoping to acquire a fast payday loan have several options. Cash advance companies operate online and offline. Local cash advance companies offer convenience. However, if you prefer privacy, applying with a local company may not offer the anonymity you desire.

On the other hand, online payday loan companies offer total privacy. In addition, you can apply for a loan in the comforts of your home or office. The entire process is completed online. When your application is approved for the loan, the cash advance company will notify you through email. Within 24 hours, the funds will be deposited into your checking or savings account.

Online payday companies may request fax copies of paycheck stubs or bank information, whereas other companies are faxless. If using an online cash advance loan company, you should review websites that offer a recommended list of reputable online payday loan companies. This way, you can compare lender fees and terms. Once you choose the perfect loan company, complete an online application, and wait for a response.

source:finance-slot.blogspot.com

Car loans make your favourite car within your reach

A car is not only a vehicle for transportation. It also reflects your attitude and desires. An exquisite design, power, and colours are some of the reasons, which make the people, crave for these vehicles. Therefore, car loans are there to help you drive your reverie car, even if you do not have enough funds to shape your dream into reality.

|

| Car Loans Source image rediff |

New cars are incredible blend of technology and innovation. Different people can have different desires regarding a car. Therefore, car loans have gained immense popularity among people as more and more people are opting for these. Due to their immense demand, various car dealers, credit unions, loan companies and some unconventional loan foundations provide car loans.

Car loans are easily available, but a lender does evaluation of borrower’s present financial situation, credit history, employment etc. Thus, it would be beneficial for a borrower to improve his credit scores because that would prove helpful in the procurement of car loans whether a borrower goes for secured car loans or unsecured car loans.

A borrower’s present financial situation and repaying capability do make him opt for secured or unsecured car loans. If he does go for secured car loans after pledging any security against the loan amount, he would enjoy some benefits. A borrower would get discount on the interest rate alongside with longer repayment period. Unsecured car loans give liberty to procure a loan without any security. These loans obtain the fast cash, but do not come with flexible terms and easier repayment options.

Car loans are like any other loans. Therefore, a borrower needs to review his credit scores and if necessary, he ought to improve these scores. Good credit scores would help to get best car loans deal. Any other information about latest car loans trend and interest rates can be acquired by shopping around or by searching on Internet.

source:finance-slot.blogspot.com

Car Title Loans Offer Risky Cash

Payday loans have received a lot of negative press lately as states and municipalities try to regulate an industry that legally lends small amounts of money at interest rates that can reach a breathtaking 1000% per year. A less well-publicized variation on the payday loan is the car title loan, which requires the borrower to provide his or her automobile as collateral for the loan amount. While this type of loan is not as widely publicized as the payday loan, the car title loan is even more dangerous, as it could cost the borrower their car!

Payday loans, also known as cash advance loans, are unsecured loans. The lender trusts the borrower to pay back the money within two weeks. This type of loan is risky for the lender, but that risk is more than offset by the high interest rates charged for the loans, which can easily top 400% on an annualized basis.

A car title loan works differently, however. With this type of loan, the borrower offers his or her car as collateral and is often asked to provide a spare set of keys when the loan is granted. Should he or she default on the loan, the car will be forfeited and sold to repay it. In some states, the lender may sell the car and keep all of the proceeds from the sale, even if they exceed the value of the loan.

With collateral, one would think that the interest rates for such loans would be far less than for payday loans, but that is not the case. Nationally, interest rates for auto title loans average about 300% per year, which hardly makes the loans a bargain. In addition, the loan amounts rarely represent more than a fraction of the value of the vehicle. A loan of even half the vehicle's value would be regarded in the industry as quite generous.

The same sorts of problems that occur with payday loans also happen with title loans. The borrower is often unable to repay on time and must extend the loan by paying an additional fee. Under some circumstances, it is possible for the fees to eventually exceed the value of the loan itself. And unlike other loans, the borrower is under pressure to avoid losing their car.

This type of loan is overwhelmingly weighted in favor of the lender, who will end up with something of far greater value than the loan should the borrower forfeit. Those who have short-term cashflow needs would be well advised to borrow from friends, relatives or a credit card instead.

source:finance-slot.blogspot.com

Dollar Car Rental Miami Are Highly A Cost Effective Means Of Commuting

Car rentals are really cost effective means of travelling. You can find many car rental agencies giving free car rental offers for travel to popular destinations. This means, you anything for renting the car, but you get to enjoy a great trip with your family or friends. You can use it to reach a really popular spot, where you can spend time the whole day. The biggest advantage you get when renting a car to travel to distant locations is choice on the type of vehicle you need. You can select an ultra-modern, large-sized vehicle that suits the occasion perfectly.

You can use the rental car to drive to locations where you cannot normally take your own vehicle. This means you can take it across difficult terrains where it is not possible to use your vehicle as it is not having features required to traverse through such places. For example, when you plan to go on long road trip in Miami, it is always best to opt for a cheap car hire service in Miami, to avoid wear and tear to your car. You might lad up with unnecessary rental costs by taking your own vehicle. A rental car will not just take you comfortably on such journeys you will spend less, which will prove to be highly economical, when you have to make more than one such long trip.

Many rental car agencies post special offers like membership offers or weekend offer, where you can find the rates slashed down by almost half. You can plan a trip that falls into their offers and enjoy the benefit of discounted rates. The rental agency always offers new car models, which are fuel efficient, thus enabling you to drive cars that give top speed and engine performance, but which also reduce your fuel costs on the journey. They will always provide well maintained cars which means you can drive a high quality car and not spend so much in terms of fuel because it will come with energy saving features.

Renting a car is highly cost effective when you dont want to take you own vehicle on a long road journey. For example, if you want to visit a scenic place just outside of Miami, hiring a car rental service in Miami can save you a lot of dollars. You can find cheap dollar car rental agencies here that give you vehicles at discount rates. They also offer special offers to loyal customers through which car rental rates can be further reduced. The next time you decide to go out on a road journey, take up reliable rental car services to cut costs and have a comfortable journey.

source:rent-infocar.blogspot.com

Considerations Before Going For Auckland Car Rental Services

When in Auckland, renting a car is the only sure and simple way of enjoying touring the city in a stress-free manner. Even though this will cost more than taking a normal ride in a bus and other public means of transport, Auckland car rental comes with several benefits that you will not manage to miss out on when visiting the city. This is by far the best option for you if you are very much conscious about comfort, freedom and flexibility since they are well designed to suit all that. Nothing however comes easy and you will have to make some considerations before getting the best car rental services in Auckland.

Have Your Priorities Right

In getting the best Auckland car rental services, you must be able to prioritize what is more important and what is less important since you cannot do everything at a go but in a systematic way. As such, determine well in advance the reasons behind your tour of the city and this will help you know whether it is worth hiring a car or not. If it's a business trip that will last for just a day, then there is no need to hire but if it's a week-long vacation, then getting a car for hire in Auckland is vital to ensure you enjoy yourself maximumly through easy movement.

You can also consider the type of car to rent depending on the places to visit. If they are rocky and hilly then a 4 wheel drive car that is strong enough is more suitable and for normal terrains, a simple car with comfort guarantee can do for you.

Choose The Right Company

You do not seek Auckland car rental services from any company you come across but you must consider the one to engage. Remember that the type of company you rent your car from will determine how you enjoy using it thus be keen to ascertain its credibility and experience in offering quality car rental services. Reputable companies will always have good services therefore make sure you go for the one with a good reputation.

If the car you are renting is to be used for a long time then you can consider including rental insurance to cover for all the damages it might be subjected to under your hands. If the company you are renting from does not have that, you can have it by yourself which is much cheaper than putting up for repair costs in case of an accident.

source:rent-infocar.blogspot.com

Choosing Between Financial Leasing And Operational Leasing When Buying A Car

Financial leasing and operational leasing are both viable options when you are leasing a car. But which one should you choose? Here we will discuss the pros and cons of each choice in order to allow you to make an informed decision.

In a financial lease, the lessee (consumer) chooses a vehicle, and then the lessor (finance company) purchases the vehicle and signs a contract with the lessee. This contract details the terms of the lease, including the length of the term, payments, interest, and any penalties that may be assessed. The finance company remains the legal owner of the vehicle until the term of the lease is up. However, the consumer is responsible for all repairs and maintenance necessary. At the end of this lease, the vehicle can either be returned to the finance company or purchased for a reduced price and becoming the legal owner of the vehicle. This is what we typically think of when we hear the term lease.

Operating leases are typically much shorter than financial leases. Another key difference is that in operational leases, the finance company is fully responsible for any maintenance or repair necessary. While this may seem ideal, there are also negative points to choosing this kind of lease. Operating leases are often more expensive per month than financial leases because the risk of owning the vehicle belongs to the finance company. They will factor in the cost of any repairs and maintenance that will need to be made, as well as protecting themselves in the event that the car is damaged. Also, you are restricted as to how much you can use the vehicle. Operating leases will dictate a set number of miles that you are allowed to drive within the lease term. If you exceed this limit, you will be charged a penalty fee. Also, at the end of an operating lease, you do not have the option to purchase the vehicle. In many ways, an operating lease is simply an extended car rental.

Both of these options have positive and negative attributes. When deciding between the two, you must think of how you plan to use the vehicle and how long you plan on keeping it. Operating leases are great for people who don t plan on spending more than a couple of years in a car. They are also great for companies who don t want to have to report a vehicle as an asset. Financial leases are ideal for people who might want to buy a specific car, but don t want to be tied down to the decision. At the end of a financial lease, if you love your car you can purchase it. If not, you simply choose another car to lease. In the end, a little bit of planning and thought can help you decide which of these types of leases is the right one for you.

source:rent-infocar.blogspot.com

Pent-up demand, stronger economy helping drive car sales in Arizona

PHOENIX – Arizonans are buying cars again due to pent-up demand, a recovering economy and favorable loan terms, according to experts.

“There are still a lot of need-buyers out there,” said Knox Ramsey, president the Valley Auto Dealers Association, noting that the average car in the U.S. at present is a higher-than-normal 11 years old.

Dennis Hoffman, an economist at Arizona State University’s W.P. Carey School of Business, said monthly sales are now around $650 million but need to be about $730 million to return the pre-recession peak.

Retail sales for both new and used vehicles in Arizona have grown about 15 percent annually for the past two years, he said.

“We’ve got a little ways to go, but the trend is certainly in the right direction,” Hoffman said.

Jim Rounds, senior vice president and senior economist at Elliott D. Pollack & Co., a Scottsdale-based consulting firm, said the growth has a lot to do with people postponing automobile purchases during the recession in order to buy necessities like food.

Maricopa County’s three-month moving average for auto purchases experienced double-digit, year-over-year growth from March 2012 through March 2013, according to Rounds’ assessment of Arizona Department of Revenue data. The area has seen growth in vehicle sales since October 2010, according to the data.

Ramsey, with the Valley Auto Dealers Association, said that while Maricopa County has seen gains across all market segments, including luxury vehicles and compact cars, dealership sales of new light trucks have been particularly strong.

Through August, new retail light-truck sales in Maricopa County grew 20.1 percent, while across the country the gain was 14.4 percent, Ramsey said.

He attributed that growth to contractors needing new vehicles because of the recovering construction market.

Registrations for all vehicles sold to individuals through Maricopa County dealerships grew 16.7 percent during the same period, while the increase just for cars was 14.1 percent, Ramsey said.

He said that the auto industry is cyclical, so he doesn’t get too excited about short-term numbers.

“It’s a real rollercoaster,” Ramsey said.

Buyers, even those with poor credit histories, also are having an easier time getting auto loans, he said.

Interest rates for a 60-month new-car loan in Phoenix ranged from 1.99 percent to 3.75 percent, according to data compiled from Bankrate.com on Monday.

Hoffman said that the rate of growth will eventually slow, though he said demand for fuel-efficient cars will continue.

People can lease cars for $200 a month that have double the fuel economy of their current vehicles, he said.

“If you’re doing a fair amount of commuting, you can offset a significant piece of that lease right from the outset,” Hoffman said.

source: cronkitenewsonline.com

Subscribe to:

Posts (Atom)